WIth the November SAAR up 1.2% year over year, to 17.5 million units, OEMs with SUV-heavy lineups fared best.

“The car-to-SUV ratio, on the month sales, were about 70% light trucks, SUVs, van, and pickups, and only 30% cars,” Edmunds Data Strategy Manager Jeremy Acevedo told Auto Finance News. “We’re seeing companies like Chrysler, who a few years ago made the transition to being an SUV- and truck-heavy lineup, lean on their Jeep and Ram brands. That’s put them ahead of the pack as far as sales go.”

While monthly sales at Fiat Chrysler increased 17%, many of the largest OEMs saw sales drop. New-car sales at Nissan, which is grappling with the arrest of the company’s Global Chairman Carlos Ghosn, dropped 18.7% in November, exceeding both Edmunds and Cox Automotive sales projections of 16.3% and 15.4% declines, respectively.

“Nissan has a twofold issue: their transition to SUVs hasn’t been as smooth as other automakers’ — the transition for a traditionally car-heavy automaker has been tough,” Acevedo said. “Nissan’s incentive spending has been pretty high. Average incentive spending for the industry is $3,976, for Nissan they’re above that at $4,556.”

Meanwhile, fleet sales were the primary driver for Kia and Subaru’s year-over-year sales increases of 1.8% and 9.8%, respectively, Acevedo said.

“Industry-wide we’ve seen a lot more fleet sales than we have in the past, but I do think that’s sustaining these growth numbers a bit,” he said. “A lot of automakers would see an even steeper year-over-year decline if there weren’t fleet numbers buoying their sales in 2018.”

The auto industry is bracing for a 25-basis-point increase in interest rates later this month, but a boost in 0% financing deals reduced average APRs in November, according to data provider Edmunds.

Average APRs on new vehicles fell to 6% in November from 6.2% in October, according to Edmunds’ Third-Quarter Used-Car Market Report. Zero percent financing offered through holiday incentives caused the dip, but analysts caution that the trend will not continue.

“Automakers are certainly offering more 0% finance deals this holiday season than they have in previous months, but they’re still few and far between,” Jeremy Acevedo, Edmunds manager of data strategy, said in a statement. “Car buyers got a bit of relief this month thanks to Black Friday deals, but an average interest rate above 6% is still a tough pill to swallow, especially for shoppers who might be coming back to the market after a number of years,” Acevedo said.

The report goes on to note that 5.5% of financing deals were 0% promos, the lowest level since November 2005. By comparison, 14.6% of financing deals in August were interest-free.

Affordability issues mount as the cost of borrowing money increases. “Used vehicles generally incur higher interest rates than new vehicles, and used-vehicle APRs continue to grow, up 11% from a year ago,” the report reads. “Consumers looking to maintain lower monthly payments are not only putting more money down as prices rise, but they’re also extending their term lengths to 66.9 months, on average.”

According to CUNA, “69% of credit union auto loans originate through the indirect channel, and only 5% of those indirect members use additional credit union products.” Once the indirect loan has been paid off, it is very difficult for the lender to extend the customer relationship. Any future engagement is with the dealer for service and maintenance.

Profitability is continually being squeezed due to steady increases in dealership fees, which have grown considerably in most markets, and in turn, reduce margins. In addition, quicker rates of pay-off, increased charge-offs and delinquencies add to profitability concerns with indirect lending. Marginal applications (not up to the institutions underwriting standards) and dealership loan documentation discrepancies further create the need to have effective oversight.

Of course, most credit unions also provide direct lending. This helps create stronger member relationships and enhances the credit union’s ability to sell other lending products to their members. However, the availability of auto loans through a credit union does not equate to increased direct lending volume.

The decision to focus on indirect lending vs. direct lending for auto loans is more than just a coin toss. For many credit unions who based the bulk of their portfolios on dealer-driven loan business, the decision to increase focus on direct lending can seem empowering. However, in order to be successful, lenders seeking to increase their direct lending portfolio will need to focus on savvy marketing, customer service, and differentiated loan offerings with consumer protection products.

Focus on Existing Members First

Credit unions are making advances with student loans, credit cards, and first mortgages. These existing members are great prospects for an auto loan. The relationship already exists, and the lender is intimately familiar with the member’s credit history. But don’t assume the member will automatically turn to you when shopping for a new vehicle!

Through direct lending, your loan officers have the opportunity to develop a one-to-one line of communication with qualified, vetted members. However, you can’t just rely on individual conversations to increase auto loan volume. Enhance that personal touch by putting into place a continuous contact strategy through email, social media, and print materials to proactively educate your members on the benefits of getting their auto loan with you. Millennial and Gen Z consumers demand online communication and will select a provider based on ease-of-use.

When it comes to differentiating your institution with both members and nonmembers, think beyond competitive interest rates and provide tangible value with consumer protection products. Products like a vehicle service contract and vehicle return protection protect the vehicle, consumer and lender in case of an unexpected vehicle breakdown or life event which could hinder timely payment.

Building a Profitable Relationship

The goal of direct lending is to gain a lifelong relationship with a new member, not just a loan. Having membership-friendly, built-in incentives for cross-sales helps generate faster on-boarding for additional services. Competitive rates, optimized consumer protection products, and a lender that understands the customer’s needs are all benefits that will pay dividends in a competitive market.

With more than 40 years of experience in the retail automotive industry, EFG can help your institution stay at the forefront of the changes affecting your industry today. Contact us today to learn how to get started.

The Senate this afternoon invoked cloture on the nomination of Kathy Kraninger as the Director of the Bureau of Consumer Financial Protection(BCFP). The 50 – 49 vote ends debate on the nomination and sets up a final vote sometime after December 4.

AFSA strongly supports President Trump‘s nomination for the Director’s position. The association submitted a letter of support to Senate Majority Leader Mitch McConnell (R-KY) and Minority Leader Chuck Schumer (D-NY) on November 19.

The letter, in part, said, “Ms. Kraninger is an excellent choice to lead the Bureau and to continue Mr. Mulvaney’s pragmatic, measured approach to ensuring that consumers benefit from safe, affordable products provided by the most responsible members of the consumer credit industry.”

Sen. McConnell filed the cloture motion required to move to Kraninger’s nomination on November 15th.

Chevrolet Bolt EV autonomous test vehicles are assembled at General Motors Orion Assembly in Orion Township, Michigan. (Photo by Jeffrey Sauger for General Motors)

General Motors’ plans to close five North American plants, cut 15% of its staff, and halt the manufacture of several car models including the Cruz, raised questions from an Edmunds analyst about how the moves will affect GM Financial.

On Nov. 26, the OEM said it was making the cuts to improve near-term performance and set itself up for a future of electronic and autonomous vehicles. But the OEM also said it was taking steps to capitalize on the future of personal mobility.

“This big transition that GM is gearing up for is transportation as a service instead of a product,” Jeremy Acevedo, manager of industry analysis at Edmunds, told Auto Finance News. “There’s not going to be a huge need for [consumers] to finance vehicles if GM is maintaining vehicles as we move toward autonomous and electric vehicles,” he said.

The idea of having a fleet of vehicles that is wholly based on utilization as opposed to ownership taps into different areas of revenue, he added, including delivery services and ride-hailing. As for the immediate-term, GM is likely to “double down on sales of high-profit SUVs and use it as a middle ground to step up financing these lofty futuristic goals,” Acevedo said.

GM said it would shut operations at plants in Detroit; Oshawa, Ontario; Warren, Ohio; White Marsh, Md.; and Warren, Mich. GM expects cash savings of $6 billion by yearend 2020.

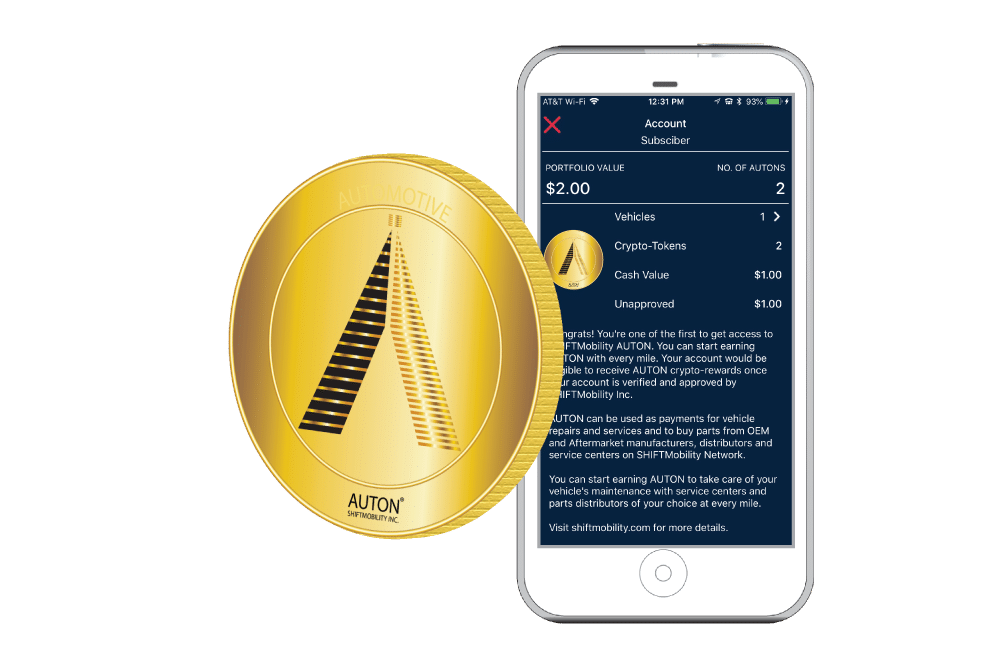

Users of a new app will soon be able to use digital currency to make payments on their loans and insurance, according to blockchain company SHIFTMobility. Come 2019, Redwood City, Calif.-based SHIFTMobility plans to incorporate lenders into its automotive ecosystem of service shops, manufacturers, and distributors, unlocking the possibility to use the partnership-wide rewards program to get discounts on loan payments.

SHIFTMobility’s lender partner program will enable users of the company’s recently released Vehicle Passport app to accrue digital tokens, called AutOns, to make insurance and loan payments.

The initial version of the app, which debuted last month, is powered by blockchain technology to consolidate specific vehicle data into a single chain – vehicle make and model, insurance, service visits, and real-time condition. The data is used to create a digital identity for any vehicle, which can be instantly shared within SHIFTMobility’s nationwide network.

“We’re able to deliver greater transparency to vehicle owners while simultaneously providing deep insight to the businesses they rely on within the automotive ecosystem,” Elliott Schendel, SHIFTMobility director of marketing, told AFN. “The inclusion of financing options is a logical step.”

So far, SHIFT has 160,000 repair shops, more than 200 parts distributors, and 200 manufacturers in the network, with some users in Canada, the U.K., and India. The company is working closely with the Virginia-based National Auto Dealers Association to further leverage blockchain adoption within the automotive industry, Schendel said.

“We are actually reinventing the automotive platforms that are used to buy new cars, used cars, the financing, and the insurance,” said Arvind Jain, SHIFTMobility CTO and co-founder. Once SHIFT builds out its lender network, consumers could accrue AutOns, currently valued at $1 each, for payments toward loans and insurance, Schendel said. “We are actively building a lender partner program for launch in 2019,” he said.

Consumers can receive AutOns based on miles driven. “As you continue to drive, because we’re capturing the data directly from the vehicles and the consumers are also participating on our network, using just a simple app like Vehicle Passport allows the consumers to save more money,” Jain said.

For instance, dealers prefer reps who are resourceful and able to get funding processed through their connections. They seek reps who are easy to reach and have the ability to get deals done for them. Good personalities are also important for reps, as is efficiency, since speedy decisioning is critical at the dealership.

Here are the five most commonly cited characteristics of reps – the traits that sway a dealer to send business to one rep over another:

Trait #1: Ability to Speed Funding.

The quicker dealers can get paid, the faster they can sell more cars. As such, reps who facilitate funding

are deemed must-haves among dealers.

For instance, one AFP respondent gauges reps on “how much effort they put in” to help with funding holdups. Another dealer sizes up reps by their “engagement” in the funding process. “Funding issues” was the most commonly cited phrase in the AFP questionnaire.

Trait #2: Friendly and Helpful Personality.

While the goal at the end of the day is to get loans funded, dealers seek reps who are pleasant, attentive, and dependable. Other sought-after personality traits include honest, professional, sincere, intuitive, and upbeat. Respondents highlighted reps who were conscientious of their time, especially during the crunch at month-end, and who exhibit “ethics and etiquette,” as one dealer said.

In addition, reps should be likeable and diligent. “I would choose the hard-working rep over the bank with the lowest rates that has no interest in building relationships with their dealers,” one respondent wrote.

Trait #3: Product Knowledge and Eagerness to Get Deals Done.

Reps’ ability to get deals done is emphasized by the dealers. To that end, dealers search out reps with a keen knowledge of their lenders’ products and services — those who can explain how their offerings are different from the competition’s. In addition, these reps should maintain strong verbal communication skills and know the ins-and-outs of their lenders’ offerings.

The more equipped a rep is with information, the greater the likelihood that the deal will progress from app to loan, and that rehashes will be completely

seamlessly. More than anything else, dealers appreciate reps who are willing to rework deals to get them bought or are willing to go above and beyond what’s required. The goal is to get to a point where dealer knows his reps are doing everything in their power to earn his business, and he feels like he can call them on any deal.

As one dealer put it, he seeks reps who “purposely go out of their way to put deals together.” Other traits that weigh into dealers’ decisions: previous F&I experience is a plus, and “knowledge of the business and how they can add to my arsenal,” according to another respondent. In a nutshell, a knowledgeable rep can trump a lower rate.

“Their tenure at a particular lender will create this knowledge and relationship that will nearly guarantee them business,” one dealer said.

Trait #4: Accessibility and Availability.

Dealers will always want to be able to reach their reps, so accessibility and availability are critical components of a strong lender-dealer relationship. Put simply, if a dealer is trying to contact a rep, but the rep is unavailable, the dealer might find another lender to do the deal instead of waiting. Some of the accessibility traits that set reps apart from their peers are those who are “easy to reach and happy to help,” or who “answer [their] cell phone, even on Sundays,” as some dealers said.

Trait #5: Be Informative.

As a lender, when you expand your product set or debut new functionality for your dealer portal, be sure that your team clearly articulates those enhancements to dealers. As we discussed in section 4, dealers expect reps to inform them about product enhancements and industry news. To that end, one dealer seeks reps who “keep us in the loop with program and deal status,” while another looks for those with “knowledge of programs and how they can benefit our business model.”

The above is a small excerpt from Auto Finance Performance’s Dealer Insights Report. The report, published by Auto Finance News’ parent company Royal Media, analyzes 6,200 dealer evaluations to identify the core traits that spur dealers to choose one lender over another. It also tracks analyst callback time and maps the frequency that dealer issues are resolved on the first call.

HyreCar, which announced earlier this month that it was expanding its service nationally, is facing a car inventory shortage, Chief Executive Joe Furnari told Auto Finance News. The car-share company added 32,000 drivers to its platform last month. Furnari said. However, he said, HyreCar has only about 720 cars available. There’s a “tremendous imbalance of drivers and cars,” Furnari said.

To alleviate its car shortage, HyreCar is looking to form more partnerships with dealers and vehicle rental companies, adding to its roster that already covers Cleveland, Dallas, New Orleans, Atlanta, among others. “We’re nowhere near saturation at this point, from the owner side and the dealer side,” Furnari said.

Among its new partnerships is a joint deal with Stork Driver PA, which rents vehicles to ride-share drives, and Reedman-Toll Auto Group, a dealer in Langhorne, Pa. Stork Driver PA will provide vehicle through HyreCar’s platform. Meanwhile, Reedman-Toll is building out a hospitality area for rideshare drivers and dedicating service bays. The new program will be located within Reedman-Toll’s 300-acre compound, which is stocked with 6,000 used-cars that will be available to rent to Uber and Lyft drivers, Furnari said.

“[Reedman-Toll Auto Group] is looking to support Lyft drivers in better ways than any other dealers have to date,” said Daryl Kessler, vice president at Reedman-Toll Auto Group, in a statement. Kessler is leading the dealer group’s initiatives. It is uncertain at press time if Reedman-Toll’s new services will be made available to both Lyft and Uber drivers.

The rating agency last week placed a tranche of notes under downgrade watch, noting that cumulative net losses (CNLs) rose to 27.2% compared with 13.4% during the past four months following the lender’s first downgraded issuance.

In July, Honor’s $112 million securitization was downgraded. Honor’s Class C notes — originally rated BB-, were downgraded to CCC+ and its portfolio subsequently acquired by Westlake Financial Services. On September 1, Westlake took over servicing from Honor, with S&P saying it believed servicing effectiveness deteriorated in July and August.

“It is not uncommon for servicing performance to decline when a servicer is being replaced — presumably a function of employees having less incentive once they become aware that a successor servicer is on the way,” S&P notes. As a result, many additional accounts were rolling into default status.

Westlake told S&P that Honor’s accounts have been difficult to service due to borrowers being accustomed to receiving extensions from Honor. While Westlake has provided some extensions since taking on the servicing role, the volume of extensions has been reduced from earlier levels. Westlake declined to comment further.

To that end, expected losses are likely to be higher than 30% given the “rapid acceleration” of losses in September and October — as well as Westlake’s expectation for a slower pace in November, S&P notes.

The level of speculative grade ABS outstandings is six times greater this year than it was in the lead-up to the Great Recession in 2006 — a stat that highlights why “caution is warranted” in subprime deals today, Amy Martin, senior director of structured finance at S&P Global Ratings, said in a September 19 webinar.

“Not only has ‘BB’ issuance doubled to $1.26 billion last year, but this is the first time we’re seeing B ratings (one grade lower than ‘BB’) to the level we are,” Martin said. “Year to date, we’ve rated $317 million in ‘B’ auto paper, and that exceeds all prior years from 2007 through 2017 combined.”

After eight straight quarters of credit tightening, lenders are widening risk parameters to reach more subprime borrowers.

The reentry into lower credit tiers stems from an increase in lenders’ use of alternative data to underwrite loans, which translates to more affordable options for subprime borrowers, said Brian Landau, senior vice president and automotive business leader at TransUnion.

Additionally, competition in the sector has diminished as some lenders retreated to the safety of prime and super-prime credit, he added.

Third-quarter subprime auto originations increased 7.3% year over year, after falling 7.8% in the prior-year period. The higher loan volume comes amid a 15-basis-point decline in delinquencies, to 6.82% as of Sept. 30.

Landau interpreted the origination growth and delinquency stabilization as signs of strength in the market, which he expects will continue through yearend.

Specifically, fourth-quarter growth will likely hinge on used-car financing and expansions in near-prime and subprime lending, Landau said.

Still, headwinds on the horizon include rising interest rates and oil prices, along with steel and aluminum tariffs.