Albany, N.Y., dealer group Keeler Motor Car Co. will debut a subscription program on May 22 to get ahead of the OEMs and captives launching their own pilot programs, Chief Executive Jesse Hord told Auto Finance News.

“We agree with the thesis that over the next five to 10 years there will be a big shift from retail to fleet,” Hord said. “We knew that the OEMs are going to start to experiment with pilots, and we wanted to figure it out for ourselves before they design the programs.” BMW Financial Services and Mercedes-Benz Financial Services both announced subscription pilots in Nashville last month, and Keeler carries both brands alongside Mini and Honda vehicles.

The dealership’s entry-level program, dubbed Drive Keeler, includes insurance, maintenance, and a combined 1,600 miles on as many as three vehicles, for $975 per month. Drive Keeler also has an “Adventure Tier” for $1,495 per month that allows for unlimited vehicle waps and mileage, as well as more luxurious cars. By comparison, Access by BMW costs between $2,000 and $3,000 per month. “Particularly in our market, where it’s very seasonal, [our consumers like] the ability to shift between a truck, a daily commuter, and have that weekend car — the date-night car,” Hord said. “The demand is there, it’s just making the economics work.” Keeler already has 80 people actively using a separate “elite membership” program it launched last year, in which customers can have loaner cars delivered.

Adding a subscription program is “the next jump for us in service levels for the customer,” Hord said. Keeler signed with Clutch Technologies for the subscription software but kept the floorplan financing in-house. “Part of our economic model is being able to finance here and capture the finance income,” he said. “If we get up to the 100- or 200-member level, we’ll do it internally and then we’ll start conversations with our bank — we have a good relationship with KeyBank — about longer-term fleet financing deals.”

DALLAS — Electric-vehicle values have been on the rise in part due to rising gas prices and greater acceptance of the technology, but the category still faces roadblocks in residual retention, panelists said at the Auto Finance Performance and Compliance Summit.

“Over the last three to six months we have seen an uptick in almost all of the EVs,” said Eric Ibara, director of residual value consulting at Kelley Blue Book. “It’s not rebounding back to where internal combustion engine is but it has ticked up.”

Gas prices have risen to a national average of $2.80 per gallon and in California — the largest state for both electric and combustion engine vehicle sales — gas is nearly a dollar more.

“If you get to that psychological hurdle of $3 per gallon nationally or $4 per gallon in California, then you could see more and more consumers going after electric vehicles and hybrid vehicles,” Anil Goyal, executive vice president of operations for Black Book National Auto Research, said during the panel discussion. “There is good demand for hybrids with gas prices going up.”

Yet, EV values are still around 20% – 30% of original MSRP after three years compared to 40% or higher for comparable combustion engines.

The exception use to be Tesla Inc. because used supply was low and the company’s marketing strategy created a lot of demand. However, as more cars slowly enter the market and the company increasingly receives more scrutiny, those advantages have waned, panelists said.

“Tesla’s [values] were retaining on par or above with some of the highest retaining vehicles out there, but that was a couple of years ago,” said Laurence Dixon, senior director of business development and valuation services at J.D. Power. “We have additional volume coming back to the market now, the aura around Tesla has started to fade away, and now residuals have come back down and fallen quite a bit from the lofty heights they initially had.”

RVI has insured electric vehicle collateral and found that the segment has over a 90% return rate after three years, largely because consumers want updated batteries with better range, said Rene Abdalah, senior vice president at RVI Group.

“Consumers want the latest and greatest every year, and that’s going to be quite common for electric vehicles,” he said. “Every year, there is going to be a new electric vehicle with bigger batteries that are cheaper.”

Positive market dynamics have prompted auto lenders to issue 12 securitizations in the first two weeks of May, a historically quiet time, Auto Finance News has learned.

The 12 transactions combined to $8.7 billion.

The top three issuances came from Toyota with an upsized amount of $1.6 billion, Ford Motor Credit with $1.5 billion, and AmeriCredit with $1.1 billion.

The other securitizers were American Car Center, Consumer Portfolio Services, Credit Acceptance Corp., First Investors Financial Services, Flagship Credit Acceptance, Westlake Financial Services, and Mercedes-Benz Financial Services, which issued two transactions.

“It’s market-driven mostly,” said Ines Beato, director of S&P Global Ratings. “Usually, it’s rates going up, or the current spreads and so on that make the timing of a deal more favorable than others.” The spread — a bond’s yield relative to the yield of its benchmark — is used both as a pricing mechanism and as a relative value comparison between bonds.

Benchmark interest rates were recently increased by the Federal Reserve in March, to a range of 1.5% to 1.75%; the Fed has signaled rates will be hiked two more times before yearend.

In a recent report from S&P on new issue volume, ABS issuance was $18 billion in April, bringing year-to-date volume to $87 billion, a 9% year-over-year increase. Of the April total, $8 billion was auto-related issuance, with $6 billion backed by prime auto loan receivables.

“Generally, there is more origination volume at the issuer level during tax season,” Beato said. “They are looking for financing on those loans, so that dictates some of the volume.” Historically, the first quarter is busier and then there’s a “lull” in the summer months, she said, adding that “we haven’t experienced that in the last couple of years.”

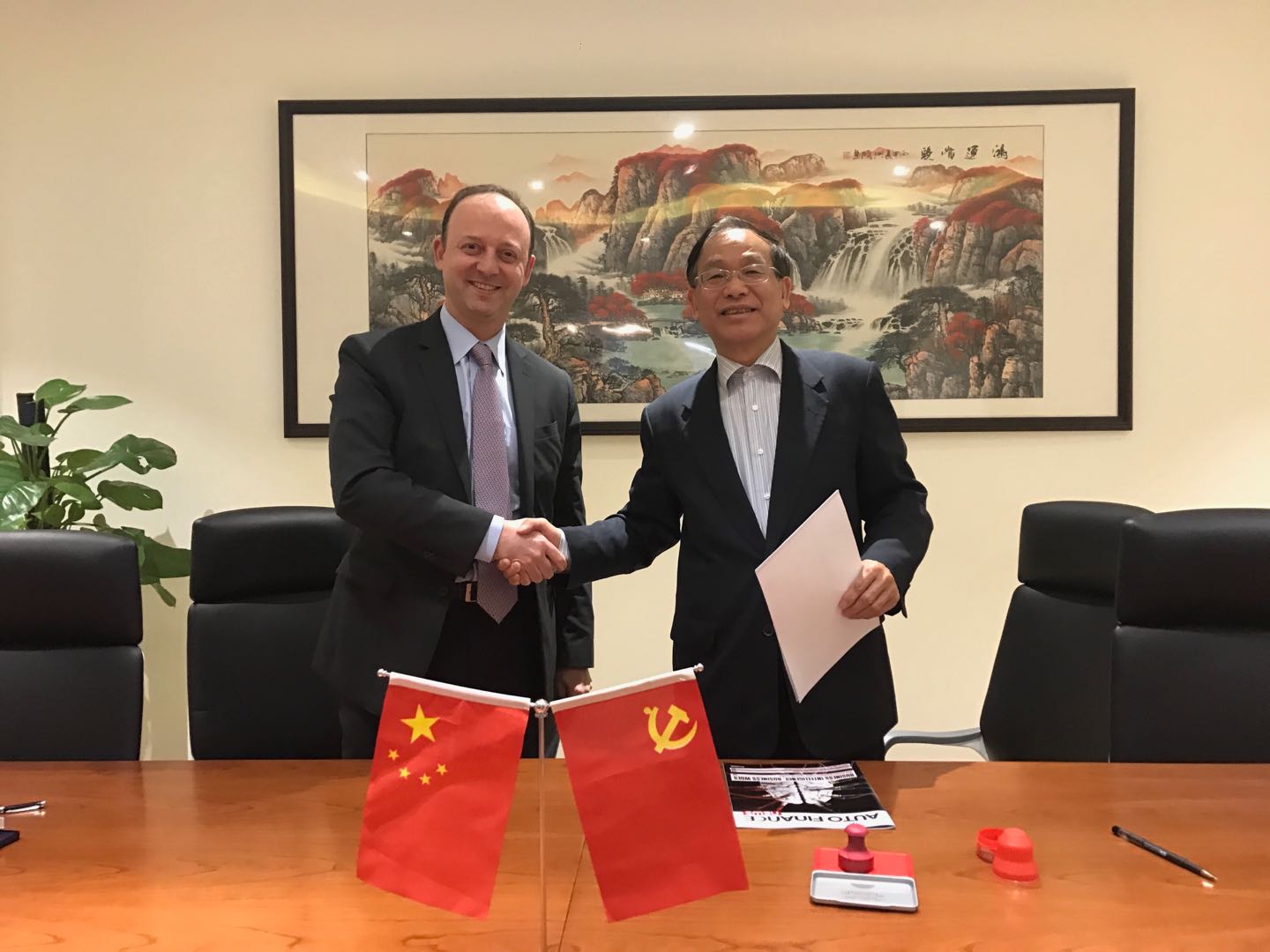

Representatives from Auto Finance News and the Shanghai Leasing Trade Association. Signing took place in Shanghai on April 25, 2018.

The Shanghai Leasing Trade Association, a non-profit association with the mission to strengthen the leasing industry’s services, self-regulation, and coordination in Shanghai, has joined Auto Finance News as the host partner for the upcoming Auto Finance Summit Asia event.

The two parties met in Shanghai on the afternoon of April 25 to formally sign an agreement. As part of its partnership, SLTA will support Auto Finance News in the execution of a new event, Auto Finance Summit Asia, which will take place September 5-6 in Shanghai. The association will work with Auto Finance News on tailoring the agenda and content for the local market, as well as inviting participation from local leasing companies.

The SLTA, which operates under the Shanghai Municipal Commission of Commerce, has more than 200 member companies. Since being founded in 1999, SLTA has made noteworthy improvements to the leasing industry and has become one of the most influential leasing trade associations in China.

“Auto finance in China is growing rapidly, and the Auto Finance Summit Asia will be a milestone event for this dynamic market,” said JJ Hornblass, Chief Executive Officer of Royal Media, the producer of the Auto Finance Summit Asia. “We are honored to be working with the SLTA to create a bridge between global auto finance markets.”

Auto Finance Summit Asia 2018 will bring the same level of expertise and professionalism as the Auto Finance Summit, Royal Media’s well-established annual event in the United States. For 17 years, Royal Media and Auto Finance News have presented the Auto Finance Summit, bringing together in the U.S. top executives in auto lending and leasing for exclusive content and unparalleled networking.

The auto finance market continued its slowdown in 2017, new data released today shows.

Yet, despite slipping originations, auto loan and lease outstandings topped $1.1 trillion in 2017 – a record high – according to the annual Big Wheels Auto Finance ranking of car lenders and lessors released today.

Big Wheels Auto Finance has been published annually since 1999.

For the seventh straight year, auto leasing gained popularity, accounting for one of every four vehicles in financiers’ portfolios. Captives — finance companies operated by car manufacturers — racked up most of the leasing gains, as they endeavored to appeal to consumers seeking lower monthly payments.

Banks, as a sector, registered minimal portfolio growth in 2017, losing marketshare to captives and credit unions. In fact, credit union outstandings grew 15% last year, the fastest clip among any institution type.

“Aside from credit unions, financiers have been backpedaling on originations, returning most of the growth recorded in 2016,” said Marcie Belles, Vice President-Auto Finance, Royal Media, and author of the report. “Heading into 2019, we expect the lending environment to weaken as credit performance worsens and profit margins are squeezed.”

Released today, the Big Wheels Auto Finance Data Report is the nation’s only ranking of the Top 100 auto financiers in the United States by originations and outstandings. The Top 5 Companies as ranked in the 2018 report, were:

Lender

2018 Rank

2017 Rank

Toyota Financial Services

1

1

Chase Auto

2

3

Ally Financial

3

2

Ford Motor Credit

4

4

GM Financial

5

7

Toyota Financial Services maintained the top spot, ending 2017 with $91.4 billion of total loans and leases outstanding and $40.3 billion of originations.

“After years of relative consistency among the nation’s largest financiers, slowing originations will likely force some industry stalwarts out of the Top 10 by yearend,” Belles said.

For the first time, the report includes access to an online data tool, allowing for seamless comparison, analysis, and data export. For an additional fee, users of Big Wheels can purchase access to 10 years of historical data — another first for Big Wheels.

China’s central government is considering regulations that would slow growth rates for financial holding companies, including auto lenders such as Ant Financial, BloombergNews reported Monday.

The government has long promoted growth but is shifting into “risk-control mode” amid concerns that Ant Financial has become too big to fail, according to the report. The proposed regulations would require any company that straddles at least two financial industries to obtain licenses from China’s central bank and meet minimum capital requirements for the first time.

China has not been entirely clear on which other companies would have to abide by these new rules, but Ant Financial competitor Tencent Holdings Ltd. — a social media platform that’s branching into financial services — is also expected to be affected.

More than 870 million customers rely on Ant Financial products including online payments, insurance, lending, credit scores, and asset management.

Last month, Chinese car retail website SouChe announced the expansion of its finance program to reach 1,700 dealerships in partnership with Ant Financial. In 2016, Ant Financial led a $100 million Series C funding round for SouChe, and in 2017 Alibaba Group Holding Ltd. led a $335 million Series E funding round to make it the largest investor in the car retail platform.

Ant Financial is an affiliate company of Alibaba. In conjunction, these three companies look to integrate business resources and incorporate Alibaba’s e-commerce, in addition, to jointly building a new retail and new finance platform for automobiles, Auto Finance Newspreviously reported.

In response to questions from Bloomberg News, representatives for Ant Financial said that its “principle has always been to work closely with regulators and support the healthy development of China’s financial sector.”

Ant Financial decline to provide additional comment to AFN.

Frontier Car Group, a Berlin-based startup that develops used-car marketplaces in developing countries, has raised $58 million in series B funding to further expand its foothold into Asia, the company announced early last week.

The funding round, which includes $41 million in equity and $17 million in debt funding, will be used to propel the business further into Africa, Latin America, and Asia. Since launching at the end of 2016, the company has sold 50,000 vehicles and is on track to do $200 million in annualized revenue per year, according to TechCrunch. Frontier Car Group currently operates in Nigeria, Mexico, Chile, Turkey, Pakistan, and Indonesia under a variety of brands Cars45.com, CarFirst, BeliMobilGue.

Frontier works by giving would-be sellers an online quote for how much their car might sell for, then Frontier inspects and buys the vehicle at that price, according to TechCrunch. Would-be buyers meanwhile use an app or web browser to shop Frontier’s stock and arrange for financing before buying the car online.

Often, these markets don’t have auction houses to get inventory and consumers are faced with a lot of fraud through classified advertising and cash deals. Frontier’s platform hopes to provide inventory and a trusted marketplace for safe used-car transactions.

Separately, Frontier is also working on new vehicle financing solutions aimed at small to medium-sized industry operators and “aspiring consumer customers in markets previously underserved by traditional lenders,” the company website says. “We’re leveraging the reach of our platform and physical network to offer innovative B2B and B2C financial products.”

Over the past few years, used-car sales have become a targeted industry for startup disruption. Carvana, the used-car platform that utilizes vehicle vending machines, went public in April 2017, Fair.com has raised over $1 billion in financing, while SouChe has made a splash in the Chinese market. But there have also been a few notables that were forced to fold such as Beepi and HelloCar in the UK.

Asia, in particular, is a strong emerging market for used-car sales. Since 2009, China has been the largest new-car market but the infrastructure for used sales has been limited. That’s starting to change Kate Gao, senior consulting manager at Ipsos Business Consulting, previously told AFN

“As new car sales peak, aftermarket (including used car) will become an important battlefield for automotive-related players,” Gao said. “From January 2017 to November 2017, China traded 11.2 million used cars, soaring by 20% year over year, and sales are expected to grow significantly in the next few years to [approximately] 21 million by 2021.”

By comparison, U.S. used-car sales hit a record 39.2 million units in 2017 — representing a 1.6% increase year over year.

Frontier did not respond to a request for comment.

New vehicles are getting more expensive, but so far those price increases have done little to dissuade consumers from pulling the trigger on new-car purchases or leases because manufacturer incentives have been so generous. However, incentives and production could be taking a downturn as auto sales slow.

Average incentive spending through February rose year over year for the 50th straight month, but there were signs of some cracks in the armor. Mainstream, non-luxury, spend fell $54 per unit during the month compared with the same period the year prior.

“That leaves premium spending as the culprit,” Tyson Jominy, director and head of PIN Consulting at J.D. Power, told Auto Finance News. Spending on luxury brands in February increased 16% year over year — or $898 per unit to $6,561 — to its highest-ever February level. The increase also marked the fourth straight month with an incentive boost greater than 15% versus the prior year, he said.

Vehicle sales are expected to slip to 16.7 million units in 2018, from 17.1 million last year. One of the primary drivers of that decline is an expectation that consumers will opt for less expensive used vehicles rather than their newer counterparts.

“Consumers may be moving into used-car financing because new-car financing is high, and new-car loan amounts have continued to grow,” said Melinda Zabritski, senior director of automotive financial solutions at Experian. “There’s more bang for your buck on the used-car side.”

New-vehicle loan amounts rose to a record high of $31,099 in the fourth quarter of 2017, up $509 year over year, according to Experian’s Automotive Finance Report. Meanwhile, even with a $300 increase in average amount financed, used vehicle prices hovered about $12,000 lower than new-vehicle prices.

It’s not just that the prices of used cars are lower than new — they always are — but financing is turning in favor of prime borrowers looking for used cars. The average interest rate for high-credit borrowers has fallen nearly 10% on used vehicles since the first quarter of 2015, according to WalletHub’s 1Q18 survey.

New-vehicle interest rates from captives averaged 1.87%, compared with 3.13% industry-wide. By comparison, used-car interest rates avareged 4.18%, WalletHub reported. This level of special rate financing can be damaging for the industry.

“There are many downstream effects of higher incentive spend, but the one we are primarily focusing on is its impact on residual values,” Jominy said. “Higher incentives lead to eroding actual, and perceived, value of vehicles, which means consumers will require longer to reach positive equity in their loans.”

“While rising transaction prices for the industry overall and reduced spending in some segments of the market is a positive indicator for the long-term health of the industry, sustaining lower levels of incentives will be challenging,” J.D. Power wrote in the report. “Considerable potential exists for spending to rise … in the months ahead.”

However, the incentive spending hasn’t been enough to stem growing interest payments as the Federal Reserve raises its rates. Captive new-car financing rose to an average rate of 1.87% in the first quarter, up from 1.77% the same period the year prior, according to WalletHub. Likewise, captive leasing rates grew to 5.13% in the quarter, compared with 4.38% in 2017.

“Given that we’re forecasting interest rates to rise even more than they are today, that’s going to make loans more expensive over their payment lifetime,” Michael Vogan, an automobile economist in the credit analytics department at Moody’s Analytics, told AFN. “As the price of cars also go up, if consumers want to keep their payment plan at the levels they are today, something has to give.”

That means either interest rates could rise, consumers could turn to cheaper but relatively new off-lease vehicles, or lenders could extend terms further out.

Average loan terms for new vehicles increased to 69 months in the fourth quarter of 2017, up from 68 months in the year-prior period, according to Experian. Meanwhile, average loan terms for used vehicles rose 0.26 months to 64 months.

“The question is, how far can [terms] go — and I think that’s an outstanding question,” Vogan said. “Banks could [increase] the net-equity risk — having the borrower be in negative equity for longer. I could see loan terms getting extended a little more, if that’s what’s required on the demand side, if that’s what consumers want.”

The Impact of Tariffs

Last month, President Donald Trump enacted a 25% tax on imported steel, which may further increase the production cost of domestic cars.

“Tariffs do have the potential of increasing the cost of producing cars in the U.S., so you could see a shift in production overseas,” Vogan said. “I don’t know what the causal chain to the finance industry would be, but it’s something the automotive industry as a whole has their eye on.”

One possible effect is an intensification of the pricing difficulties already outlined above. More expensive cars mean lenders and manufacturers have to come up with new ways to lower monthly payments for consumers.

OEMs could reduce production to mitigate pricing pressures, but those plans are already underway due to the excess off-lease volume in the market.

“You have to provide a lot of incentives because there’s so much competition from the off-lease volume, which is forecasted to peak in 2020,” Vogel said. “Going forward, you’re already coming down off that peak. From an off-lease volume perspective, I don’t think the production adjustments are going to help mitigate any price pressures we’ll see over the next three years.”

Via funcityfinder.com

Increased Competition From Credit Unions

Incentives could also be on the rise as captives feel the pressure from credit unions, Experian’s Zabritski said.

“As we see these rate increases, we’ll see more incentives coming out of the captives to remain competitive and drive sales,” she said. “Certainly, as you have rate increases, credit unions have some advantages: They have a different cost of funds, they operate in a different competitive environment, and they operate in a different regulatory environment.”

Credit union marketshare grew 200 basis points year-over-year to 21.1% of the market in the fourth quarter. Meanwhile captives were able to grow at a similar clip to 29.9% of the market in the fourth quarter, up from 28.4% the same period the year prior.

More prime consumers are expected to choose used vehicles over new in 2018, and credit unions are poised to offer the best rates to those consumers, Zabritski said.

“Credit unions tend to finance much more heavily in used vehicles, especially compared to captives that are mostly new,” she said. “The credit unions are picking up marketshare left and right, and really expanding in the marketplace. They aren’t that far behind the banks in the used-car industry.”

Four auto manufacturers have teamed up with technology companies to form a new consortium dedicated to exploring the use of blockchain technology in mobility ecosystems that could make transportation safer, more affordable, and more widely accessible, the companies jointly announced Wednesday.

BMW, Ford, General Motors, and Groupe Renault joined in with 37 other companies — among them, technology leaders such as Bosch and IBM — to form the Mobility Open Blockchain Initiative (MOBI)

Blockchain technology works by distributing information to a network of independent computers. Because of this decentralized system, data privacy, ownership rights, and integrity are protected and transactions are more secure. Some of the consortium’s projects include secure vehicle payments, mobile commerce, vehicle data tracking, and usage-based mobility pricing, car payments, and insurance.

“Working in a consortium allows MOBI and partners to create transparency and trust among users, reduce risk of fraud, and reduce frictions and transaction costs in mobility, such as fees or surcharges applied by third-parties,” the announcement said.

Chris Ballinger, former chief financial officer and director of mobility services at the Toyota Research Institute, left his position with the OEM recently to found MOBI as its chairman and chief executive, according to the consortium’s website.

MOBI appears to be an evolution of Blockchain Mobility Consortium that launched in 2017, Internet of Business pointed out. Toyota Research Insitute launched its own consortium in May 2017 and joined the Enterprise Ethereum Alliance consortium that same time, in addition to participating in R3.

This is not the first time that automakers have expressed interest in working with blockchain either. GM Financial and Daimler AG joined Hyperledger late last year. Hyperledger is one of the 37 companies joining MOBI and its Executive Director Brian Behlendorf, has joined MOBI’s board of advisors.

Through an open-source approach to blockchain software tools and standards, the MOBI consortium hopes to stimulate more rapid and scalable adoption of the technology by other companies developing autonomous vehicle and mobility services. Initially, MOBI will be working with its partners on projects related to vehicle identity, history and data tracking, autonomous machine and vehicle payments, car sharing, ride-hailing, and more.

How involved automotive captives are, if at all, in the consortium is not entirely clear, although BMW Spokesman Michael Ortmeier said BMW Financial Services is not involved. Yet, it is telling that Ballinger — who spent 14 years at Toyota Financial Services before leading the OEM’s mobility efforts — is leading the consortium.

“The BMW Group, along with other OEMs, signed a non-binding memorandum of understanding to participate in the Mobility Open Blockchain Initiative,” Ortmeier said, adding, “In the future, there is a possibility to get involved financially in order to take on chair positions in the governing body and take an active role within the community to create favorable standards and secure access to the latest emerging technologies.”

Ford and Group Renault did not respond to requests for comment by press time.

Credit Acceptance Corp. grew its origination volume 18.5% year over year in the first quarter but continues to forecast lower collection rates for the loans it’s originating, the company reported in earnings today.

The company originated 112,345 auto loans in the first quarter ending in March, up from 94,809 the same period the year prior. Credit Acceptance also noted volume growth of 25.3% in April alone.

However, Credit Acceptance expects to collect on just 63.6% of the amount owed on that pool of loans — the lowest initial forecast it’s posted in the past nine years.

As a result, more of Credit Acceptance’s dealer partners are opting for up-front cash deals as opposed to relying on income from collections on the loans over time. Nearly 30% of the lender’s loan volume was from its purchased loans program — which only offers a cash advance to dealers — compared with 27% the same period the year prior.

Still, Credit Acceptance is growing its dealer base with 911 more active dealers in the first quarter than it had the same period the year prior. The average dealer in that network sold 12.8 loans in the quarter up from 12.1 in the comparable quarter.

Despite these lower collection rates, Credit Acceptance brought in $71.5 million in profit for the quarter up from $58.5 million the same quarter the year prior.

“Forecasting collection rates accurately at loan inception is difficult,” the company said in the report. “With this in mind, we establish advance rates that are intended to allow us to achieve acceptable levels of profitability, even if collection rates are less than we initially forecast.”

Additionally, Credit Acceptance is funding larger loan amounts at longer terms. The average amount financed rose 7.3% year over year to $21,719. Average loan terms extended to 57 months long in 2018, up two months longer than in 2017.